The Trump administration's trade policies and tariffs reduced U.S. income at a rate of $1.4 billion per month by the end of last November, according to new research from the Federal Reserve Bank of New York, Princeton University and Columbia University.

The collaborative study found that U.S. businesses and consumers saw "substantial increases" in the price of goods throughout last year, including a "complete passthrough" of U.S.-imposed tariffs onto imported items. The economists — the New York Fed's Mary Amiti, Princeton professor Stephen Redding and Columbia professor David Weinstein — also said Americans suffered by a lack of import variety and disruptions to supply chains.

"Economists have long argued that there are real income losses from import protection. Using the evidence to date from the 2018 trade war, we find empirical support for these arguments," the researchers wrote. "Losses mounted steadily over the year, as each wave of tariffs affected additional countries and products, and increased substantially after the imposition of the wave 6 tariffs on $200 billion dollars of Chinese exports."

Amiti, Redding and Weinstein found that while losses were accumulating at a rate of $1.4 billion per month by last November, total losses from January 2018 through November 2018 ballooned to a conservative estimate of $6.9 billion.

That number may be too low, the economists said, because their model assumes that the U.S. government uses tariff tax revenues to offset the welfare burden. If the U.S. government did not offset the cost of the tariffs to the American consumer with the new tax revenues, the full value of the tariff payments would be $12.3 billion.

The White House imposed a variety tariffs on goods imported from economic partners of the U.S. in 2018. The tit-for-tat between the U.S. and China has come as Trump and the U.S. Trade Representative try to protect American intellectual property and curb a steep trade deficit.

Trump has had varying success with the tariff tactic, winning both a revised version of the North American Free Trade Agreement as well as alienating key allies including Canada and the European Union. The White House announced a round of tariffs on $200 billion of products imported from China at a 10 percent rate last year.

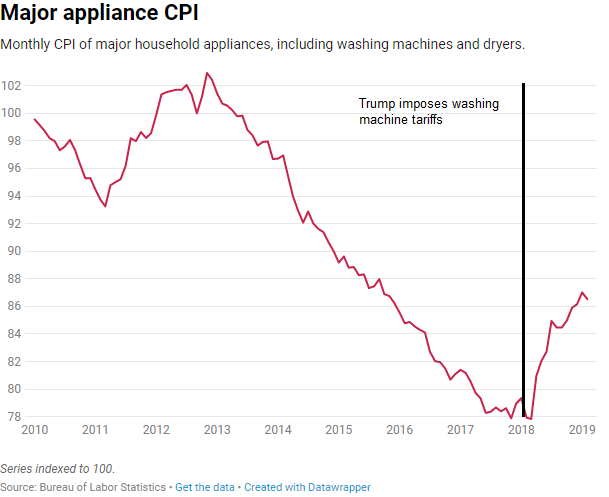

The White House also announced last year the introduction of a 20 percent tariff on the first 1.2 million imported large residential washing machines from South Korea in the first year and a 50 percent tariff on machines above that number. LG Electronics told retailers less than one week after that decision that it would hike prices thanks to Trump's protective policy.

Less varietyThe research team also found that American consumers are also harmed during a trade war in terms of the variety of goods they can purchase. Consumers benefit from open trade and the ability to purchase more unique goods — like French wine and Colombian coffee, for example — that might be foregone if trade barriers are high.

In the three years prior to the imposition of tariffs, all categories of goods experienced increases in the number of varieties offered in the U.S., the researchers said.

"However, the imposition of the tariffs is associated with sharp drops in the number of imported varieties entering the U.S. in all sectors except the wave 1 products (washing machines and solar panels)," they wrote.

"These results suggest that some of the tariffs were prohibitive, reducing imports to zero. This can create a measurement problem that can arise if we try to assess the price impacts of tariffs on goods that are no longer imported."

The trade war also caused "dramatic" turmoil in supply chains, as about $165 billion of trade ($136 billion of imports and $29 of exports) is lost or redirected through company and customer efforts to circumvent tariffs.

"We find that the U.S. tariffs were almost completely passed through into U.S. domestic prices, so that the entire incidence of the tariffs fell on domestic consumers and importers up to now, with no impact so far on the prices received by foreign exporters," the Fed, Princeton and Columbia economists wrote. "We also find that U.S. producers responded to reduced import competition by raising their prices."