China’s currency has had a bumpier ride in the past several weeks than it’s seen since it stabilized against the dollar in 2017, and further turbulence may be in store as companies prepare to make a welter of dividend payments abroad.

Offshore-listed Chinese firms will hand out $19.6 billion of dividends in overseas currencies in the three months through August, according to data compiled by Bloomberg. While some of the payments will be made from existing foreign-exchange holdings, some conversions from yuan will be needed, contributing to volatility, market players say.

Dollars WantedChinese companies will buy more foreign-exchange for dividend payments

Bloomberg

.chart-js { display: none; }After a long stretch of gains from 2017 to early 2018, the yuan lately has been confronting a resurgent dollar, thanks to rising U.S. Treasury yields. China’s currency dropped the most since 2016 last month, when its foreign-exchange reserves saw the first back-to-back drop in more than a year. On the flip side, depreciation has been limited by overseas investors’ increasing interest in Chinese securities, with net bond inflows the past 15 straight months.

Top 10 China Stocks To Watch For 2019: Focus Media Holding Limited(FMCN)

Advisors' Opinion:- [By Stephan Byrd]

An issue of Focus Media Holding Limited (NASDAQ:FMCN) debt fell 1.1% against its face value during trading on Tuesday. The debt issue has a 7.5% coupon and is set to mature on April 1, 2025. The debt is now trading at $97.63 and was trading at $98.50 last week. Price changes in a company’s debt in credit markets sometimes anticipate parallel changes in its stock price.

- [By Stephan Byrd]

An issue of Focus Media Holding Limited (NASDAQ:FMCN) bonds fell 0.9% against their face value during trading on Monday. The high-yield debt issue has a 7.25% coupon and will mature on April 1, 2023. The bonds in the issue are now trading at $99.13 and were trading at $98.13 last week. Price moves in a company’s bonds in credit markets sometimes anticipate parallel moves in its share price.

Top 10 China Stocks To Watch For 2019: Sina Corporation(SINA)

Advisors' Opinion:- [By Ethan Ryder]

Get a free copy of the Zacks research report on SINA (SINA)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Leo Sun]

But as the U.S. market remains stuck in neutral, Chinese tech stocks have thrived, sparked by impressive growth figures and their detachment from U.S.-centered issues. Let's examine three stocks in that industry which have already rallied more than 30% this month -- Baozun (NASDAQ:BZUN), Weibo (NASDAQ:WB), and SINA (NASDAQ:SINA).

- [By Ethan Ryder]

Eagle Global Advisors LLC decreased its position in Sina Corp (NASDAQ:SINA) by 1.8% during the 1st quarter, according to the company in its most recent disclosure with the Securities & Exchange Commission. The institutional investor owned 84,875 shares of the technology company’s stock after selling 1,595 shares during the period. Eagle Global Advisors LLC owned about 0.12% of Sina worth $8,850,000 at the end of the most recent quarter.

- [By Steve Symington]

You wouldn't know it by the market's knee-jerk reaction, but SINA Corp. (NASDAQ:SINA) just announced another stronger-than-expected quarter early Wednesday. Shares of the Chinese internet media company fell 10% when all was said and done today -- though it's not the first time we've seen the stock fall on positive news.

- [By Lisa Levin] Gainers Cocrystal Pharma, Inc. (NASDAQ: COCP) rose 15.3 percent to $2.41 in pre-market trading after declining 25.09 percent on Thursday. Expedia Group, Inc. (NASDAQ: EXPE) shares rose 10.7 percent to $117.75 in pre-market trading after the company reported stronger-than-expected earnings for its first quarter on Thursday. DMC Global Inc. (NASDAQ: BOOM) rose 10.6 percent to $35.00 in pre-market trading after reporting Q1 results. Genprex, Inc. (NASDAQ: GNPX) rose 10.2 percent to $12.12 in pre-market trading after climbing 86.76 percent on Thursday. Sprint Corporation (NYSE: S) shares rose 7 percent to $6.42 in pre-market trading on reports that the company has made progress on merger talks with T-Mobile. Amazon.com, Inc. (NASDAQ: AMZN) rose 6.9 percent to $1,621.95 in pre-market trading after the company posted upbeat results for its first quarter. The company sees second quarter operating income of $1.1 billion - $1.9 billion and sales of $51 billion - $54 billion. Riot Blockchain, Inc. (NASDAQ: RIOT) shares rose 5.5 percent to $7.88 in pre-market trading after gaining 1.49 percent on Thursday. Intel Corporation (NASDAQ: INTC) rose 5.3 percent to $55.86 in pre-market trading as the company reported better-than-expected results for its first quarter and also raised its FY18 sales outlook. 8x8, Inc. (NASDAQ: EGHT) rose 5.3 percent to $21.00 in pre-market trading. Southwestern Energy Company (NYSE: SWN) shares rose 5.1 percent to $4.75 in pre-market trading as the company reported better-than-expected earnings for its first quarter. Diamond Offshore Drilling, Inc. (NYSE: DO) rose 5 percent to $20.24 in pre-market trading. Baidu, Inc. (NASDAQ: BIDU) rose 4.5 percent to $249.50 in pre-market trading following upbeat Q1 profit. Charter Communications, Inc. (NASDAQ: CHTR) rose 4.3 percent to $311 in pre-market trading. Charter is expected to release quarterly earnings today. SINA Corporation (NASDAQ: SINA) shares rose 3.9 pe

- [By Shane Hupp]

SINA Corp (NASDAQ:SINA) shares hit a new 52-week low on Wednesday . The stock traded as low as $83.39 and last traded at $82.78, with a volume of 41597 shares trading hands. The stock had previously closed at $85.15.

Top 10 China Stocks To Watch For 2019: Baidu Inc.(BIDU)

Advisors' Opinion:- [By Motley Fool Staff]

Dylan Lewis: This property just got spun out of Baidu (NASDAQ:BIDU) fairly recently. Shares have not been trading all that long. And in that time, we've seen the usual fluctuations that you might expect from a new issuance hitting the public markets. Some of that is due to some recent developments that are helping the company out.

- [By ]

Believe it or not, Chinese firms like internet giant Baidu (Nasdaq: BIDU) may make significant investments to fight the currency threat. The reason being is that the company boasts more cash than debt and will continue to grow thanks to China's expanding middle-class despite the pending tariffs.

- [By ]

LexinFintech Holdings Ltd. (LX) : "The only ones I'm recommending from China are Baidu.com (BIDU) , Alibaba (BABA) and Baozun (BZUN) ."

Illinois Tools Works (ITW) shares fell after the company's earnings report, but Cramer and the AAP team see it as an opportunity to buy more shares. Find out what they're telling their investment club members and get in on the conversation with a free trial subscription to Action Alerts PLUS.

- [By ]

Earlier this year, Bank of America estimated that between them, Google, Facebook, Amazon, Microsoft (MSFT) , Alibaba (BABA) , Baidu (BIDU) and Tencent would grow their capex by 30% in 2018 to $74.1 billion. Google, it should be noted, just spent much more on capex in Q1 than the $3.4 billion BofA expected it to spend.

Top 10 China Stocks To Watch For 2019: ATA Inc.(ATAI)

Advisors' Opinion:- [By Paul Ausick]

ATA Inc. (NASDAQ: ATAI) traded down about 14% Monday to set a new 52-week low of $0.82, based on revalued shares that closed at $0.72 on Friday but traded up about 250% on Monday at $2.53. Volume was more than 200 times the daily average of around 42,000. You’re on your own here to figure this one out.

Top 10 China Stocks To Watch For 2019: Clean Diesel Technologies Inc.(CDTI)

Advisors' Opinion:- [By Logan Wallace]

Shares of CDTi Advanced Materials Inc (NASDAQ:CDTI) hit a new 52-week low during mid-day trading on Wednesday . The stock traded as low as $0.33 and last traded at $0.36, with a volume of 500 shares trading hands. The stock had previously closed at $0.36.

- [By Stephan Byrd]

Here are some of the media stories that may have impacted Accern Sentiment’s analysis:

Get Molecular Templates alerts: Trading Center: Watching the Levels for Molecular Templates, Inc. (:MTEM): Move of 0.02 Since the Open (stocknewscaller.com) Molecular Templates (MTEM) Announces Clinical Data at 2018 ASCO Meeting (streetinsider.com) Gallbladder Cancer Treatment Sales Market Size by Players, Regions, Type, Application and Forecast to 2025 (exclusivereportage.com) ATR in spotlight EnSync, Inc. (NYSE:ESNC), CDTi Advanced Materials, Inc. (NASDAQ:CDTI), Molecular Templates, Inc … (stocksnewspoint.com)MTEM has been the subject of several research analyst reports. ValuEngine lowered shares of Molecular Templates from a “hold” rating to a “sell” rating in a research report on Thursday, March 1st. Zacks Investment Research raised shares of Molecular Templates from a “sell” rating to a “hold” rating in a research report on Thursday, June 7th. Four analysts have rated the stock with a hold rating and one has given a buy rating to the stock. The company has a consensus rating of “Hold” and an average price target of $5.20.

Top 10 China Stocks To Watch For 2019: Top Image Systems Ltd.(TISA)

Advisors' Opinion:- [By Ethan Ryder]

Get a free copy of the Zacks research report on Top Image Systems (TISA)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Money Morning Staff Reports]

Before we get to our latest pick, here are last week's top-performing penny stocks:

Penny Stock Sector Current Share Price Last Week's Gain Melinta Therapeutics Inc. (NASDAQ: MLNT) Healthcare $1.74 104.01% Pernix Therapeutics Holdings Inc. (NASDAQ: PTX) Healthcare $0.83 84.40% Top Image Systems Ltd. (NASDAQ: TISA) Healthcare $0.82 59.85% Jason Industries Inc. (NASDAQ: JASN) Healthcare $2.21 58.99% Maxwell Technologies Inc. (NASDAQ: MXWL) Financial $4.66 51.79% Marathon Patent Group Inc. (NASDAQ: MARA) Healthcare $0.52 51.47% Forward Pharma A/S (NASDAQ: FWP) Basic Materials $1.53 43.57% Dixie Group Inc. (NASDAQ: DXYN) Healthcare $1.40 42.86% Trevena Inc. (NASDAQ: TRVN) Services $1.41 39.60% Alliance MMA Inc. (NASDAQ: AMMA) Healthcare $4.95 36.18%Don't Miss Out: The Treasury is sitting on an $11.1 billion cash pile, and a loophole entitles Americans to a sizable portion. Some are collecting $1,795, $3,000, or $5,000 every month thanks to this powerful investment…

- [By Joseph Griffin]

Get a free copy of the Zacks research report on Top Image Systems (TISA)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

Top 10 China Stocks To Watch For 2019: Renesola Ltd.(SOL)

Advisors' Opinion:- [By Joseph Griffin]

These are some of the media headlines that may have impacted Accern’s scoring:

Get ReneSola alerts: ReneSola Sells North Carolina Solar Project To Greenbacker (solarindustrymag.com) ReneSola (SOL) Rating Increased to Neutral at Roth Capital (americanbankingnews.com) ReneSola (SOL) Q1 Earnings in Line, Revenues Top Estimates (zacks.com) ReneSola’s (SOL) CEO Xianshou Li on Q1 2018 Results – Earnings Call Transcript (seekingalpha.com) ReneSola (SOL) Releases Earnings Results (americanbankingnews.com)Shares of ReneSola traded up $0.08, hitting $2.76, during trading on Friday, Marketbeat.com reports. The stock had a trading volume of 124,969 shares, compared to its average volume of 108,565. The firm has a market capitalization of $102.11 million, a PE ratio of 21.23 and a beta of 2.05. The company has a current ratio of 1.17, a quick ratio of 1.17 and a debt-to-equity ratio of 0.36. ReneSola has a 12 month low of $2.12 and a 12 month high of $3.79.

- [By Logan Wallace]

Get a free copy of the Zacks research report on ReneSola (SOL)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Max Byerly]

Sola Token (CURRENCY:SOL) traded 17.9% lower against the dollar during the 1-day period ending at 16:00 PM E.T. on October 11th. One Sola Token token can now be bought for about $0.0054 or 0.00000087 BTC on cryptocurrency exchanges including Tidex and OpenLedger DEX. Sola Token has a total market cap of $153,306.00 and $1,856.00 worth of Sola Token was traded on exchanges in the last 24 hours. In the last seven days, Sola Token has traded down 12.2% against the dollar.

- [By Max Byerly]

Sola Token (CURRENCY:SOL) traded up 26.7% against the US dollar during the 24 hour period ending at 22:00 PM E.T. on September 28th. One Sola Token token can currently be bought for $0.0085 or 0.00000131 BTC on popular exchanges including Tidex and OpenLedger DEX. Sola Token has a market capitalization of $0.00 and approximately $3,239.00 worth of Sola Token was traded on exchanges in the last 24 hours. During the last week, Sola Token has traded flat against the US dollar.

Top 10 China Stocks To Watch For 2019: Netease.com Inc.(NTES)

Advisors' Opinion:- [By Lisa Levin]

NetEase, Inc. (NASDAQ: NTES) is expected to post quarterly earnings at $2.19 per share on revenue of $2.18 billion.

China Distance Education Holdings Limited (NYSE: DL) is estimated to post earnings for its second quarter.

- [By Joseph Griffin]

Here are some of the media headlines that may have effected Accern Sentiment’s analysis:

Get NetEase alerts: Marvel Introduces Their First Official Chinese Superheroes (huffingtonpost.com) NetEase, Inc. (NTES) year to date performance remained at -22.66% (nasdaqfortune.com) Marvel get its first official Chinese superheroes (bbc.co.uk) Why to Follow this Stock? NetEase, Inc. (NTES) (nysestocks.review) Marvel’s first Chinese superheroes are coming—and here are their superpowers (quartzy.qz.com)A number of research firms recently weighed in on NTES. BidaskClub cut NetEase from a “hold” rating to a “sell” rating in a report on Tuesday, March 27th. Jefferies Group reduced their price target on NetEase from $335.00 to $310.00 and set a “hold” rating for the company in a report on Tuesday, April 10th. CLSA raised NetEase from a “sell” rating to an “underperform” rating in a report on Thursday, February 8th. Zacks Investment Research raised NetEase from a “sell” rating to a “hold” rating in a report on Thursday, March 8th. Finally, JPMorgan Chase began coverage on NetEase in a report on Thursday, April 12th. They issued an “underweight” rating and a $240.00 price target for the company. Five research analysts have rated the stock with a sell rating, four have given a hold rating, eight have given a buy rating and one has assigned a strong buy rating to the company’s stock. NetEase currently has a consensus rating of “Hold” and a consensus price target of $337.47.

- [By Dan Caplinger]

The stock market gave up ground on Thursday, with the Dow Jones Industrial Average falling triple digits and other major market benchmarks following suit with declines of close to 0.5%. Investors seemed inclined to take their foot off the gas after the strong start to the year, as fears about possible deterioration in economic strength and the geopolitical climate weighed on sentiment. Bad news from some high-profile companies also hurt the overall market. Domino's Pizza (NYSE:DPZ), Carbon Black (NASDAQ:CBLK), and NetEase (NASDAQ:NTES) were among the worst performers. Here's why they did so poorly.

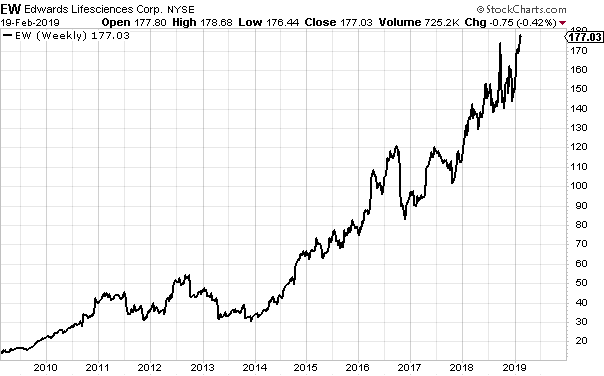

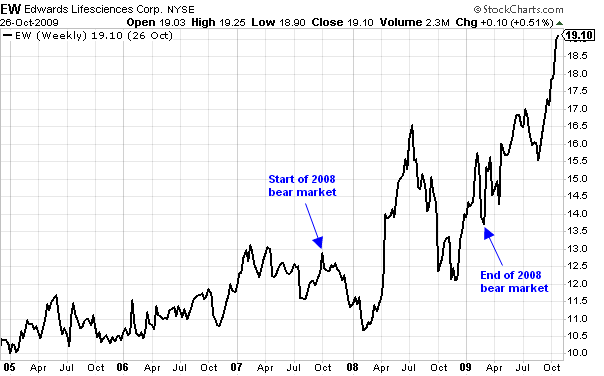

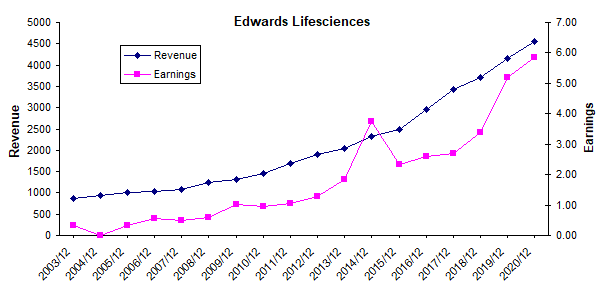

Edwards Lifesciences data by ADVFN

Edwards Lifesciences data by ADVFN