Edwards Lifesciences Corp. (NYSE:EW) provides products used to treat heart disease and critical care monitoring. The company's products are available in the United States and internationally.

Edwards Lifesciences has a solid history of earnings growth with a boost to earnings expected for 2019 due to the release a new medical software product. The company is efficiently run, and management actively seeks out opportunities to further increase its earnings.

The stock is expensive with high PEG and PE multiples, but it's essentially recession-proof by the nature of its products, which are considered to be essential. In my opinion, Edwards Lifesciences would make a great long-term investment.

FinancialsEdwards Lifesciences has reported full year financial results for 2018 (data from Seeking Alpha and Yahoo).

The reported revenue was up 8.1 percent over the 2017 fiscal year, and earnings were up 24 percent. Over the last five years, Edwards Lifesciences' revenue has grown 9.9 percent per year, and its gross income increased by 10.6 percent per year.

The return on equity is very good at 24 percent, and the profit margin (profit to revenue ratio) is strong at 20 percent. These have been fairly consistent over the last decade.

Edwards Lifesciences' current ratio is 2.6, which means the company has a surplus working capital (which means that the company can easily pay its bills without needing any long-term financing). Over the last ten years, its current ratio has always been above 2.

The total debt ratio (total liabilities to total assets) is 40 percent, which means that Edwards Lifesciences' total debt is only 40 percent of the value of everything the company owns (note that the asset value is the book value and not the liquidated value of its assets).

The company's book value is currently around $15, and with a stock price of $177, Edwards Lifesciences is trading at 11.7x book value.

The analysts' consensus forecast is for revenue to increase by 10.0 percent in 2020, and earnings are forecast to increase 12.3 percent in 2020. The 2020 PE ratio is 30x.

The financials reveal that Edwards Lifesciences is an efficiently run company with plenty of working capital. The company operates with a decent profit margin and generates a good return on equity. The company's debt level is moderately low, and if needed, Edwards Lifesciences could easily take on more debt.

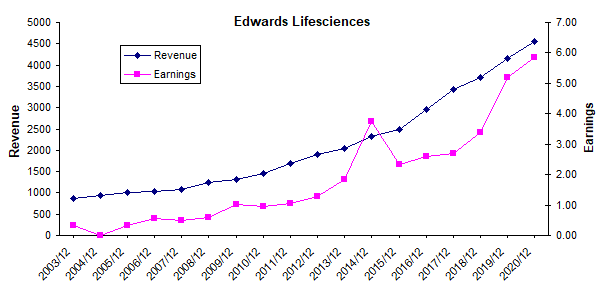

Revenue and EarningsAs an investor, I personally like to examine the company's historical revenue and earnings trends. To make this task easier and to highlight trends, I like to visually display the data on a graph.

Edwards Lifesciences data by ADVFN

Edwards Lifesciences data by ADVFN

The above chart visually shows Edwards Lifesciences' revenue and earnings historical trend along with the next two years of consensus forecasts.

Examining the chart shows that Edwards Lifesciences' revenue has steadily increased over the last 15 years. The forecast revenue growth for 2019 and 2020 is in line with its historical growth trend. The company's earnings have also increased along with its revenue. The company did report very high earnings for the 2014 fiscal year, but this included a once off abnormal credit. On a gross income basis, the 2014 profit is in line with its historical trend. The forecast earnings for 2019 does show a jump up, but it's still broadly in line with its growth trend. The 2020 earnings forecast continues along with its growth trend.

The chart shows me that Edwards Lifesciences is a company with strong historical growth trends. While the analysts' 2019 earnings could be a little optimistic, they are a consensus average of 23 analysts.

The future always holds uncertainties, and forecasting is really nothing more than projecting forward what's currently happening. What I do know as fact is that Edwards Lifesciences has an established history of growth, and unless something dramatic happens in the future, I feel confident that this growth will continue into the future.

In Edwards Lifesciences' Earnings Call, Mike Mussallem - Chairman and CEO stated,

We believe there are a large number of patients suffering from aortic stenosis who are either undiagnosed or untreated. We're investing in programs to increase awareness, increase diagnosis, improve referral patterns and help patients receive the care they need based on medical guidelines.

Now, this is what I like to hear from management - future opportunities! Now, not to sound morbid, but the company has identified a medical condition with cases that aren't being treated. This is an opportunity for the company to market its treatments to patients who really should be using it (and thereby providing an increased revenue source). This is what I call proactive management.

Mike Mussallem made two more statements,

We continue to see excellent long term opportunities for growth as we believe international adoption of TAVR therapy is still quite low.

We are committed to maintaining our leadership in TAVR, which remains a large global opportunity that we estimate will double in size and reach approximately $7 billion by 2024.

Again, there is more potential for revenue growth here as the company sees an expanding market internationally for its TAVR (Heart Valve) therapy.

Mike Mussallem further stated that they had received FDA clearance for their Acumen Hypotension Prediction Index software, which is expected to provide a strong growth driver for 2019. Now, this explains why the analysts had bumped up the company's 2019 earnings growth forecast - there's a new software product to boost earnings for 2019.

In my opinion, management is proactive, and I feel confident that Edwards Lifesciences' revenue and earnings will continue to grow for many years to come. The company's products are essential items and services that patients with heart conditions need. This suggests that Edwards Lifesciences' earnings would be largely shielded during periods of economic weakness, making the company essentially recession-proof.

Stock ValuationAs Edwards Lifesciences is a growth stock, the PEG (PE divided by the earnings growth rate) is an appropriate valuation method.

Edwards Lifesciences' gross income increased 10.6 percent per year over the last five years. The forward annual earnings are for increases of 53 percent in 2019 and 12.3 percent in 2020.

The bump up in 2019 earnings was probably due to its new software release for 2019, which is expected to drive up earnings in that year.

Given that historical revenue growth is 12.5 percent per year, I would use the forecast 2020 earnings growth rate of 12.3 percent, which results in a forward PEG of 2.5 with a 2020 PE multiple of 30x.

It's commonly accepted that a stock is fairly valued when its forward PEG is 1.0, which means that Edwards Lifesciences is overvalued with a stock price of $177. Its fair value would be around $70.

On a PE basis, Edwards Lifesciences is trading at a high 30x for its 2020 estimated earnings, and its book value is 11.7x. While Edwards Lifesciences is overvalued, most good growth stocks are expensive as the stock market is prepared to pay a premium for earnings growth.

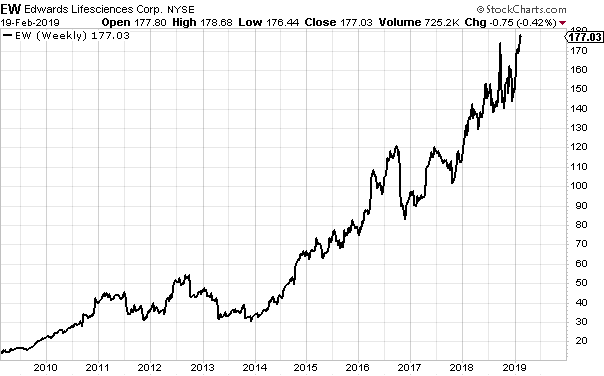

Stock Price TargetAs an active investor, I personally like to determine some likely price targets. This gives me a feel for how high the stock price could go in the short term and how soon it could get there.

Edwards Lifesciences chart by StockCharts.com

The stock chart reveals that Edwards Lifesciences has increased considerably over the last decade - especially since the start of 2014. The stock ran up to peak in mid-2018 and then pulled back as the market showed weakness in the latter half of 2018. The stock then rallied this year along with the stock market to trade at a new high.

Should the market continue to rally, then I would expect Edwards Lifesciences to follow. The rally seen in 2018 could be replicated in 2019. The 2018 rally was from $115 to $150. This $35 rally added to the $150 at the start of 2019, which gives a target of $185. Granted that the stock has almost reached $185, but history shows that the stock will likely pullback and rally and repeat this several times during 2019.

Over the longer term, the stock could trade well past the 2018 high and will probably do so as long as Edwards Lifesciences' earnings growth continues.

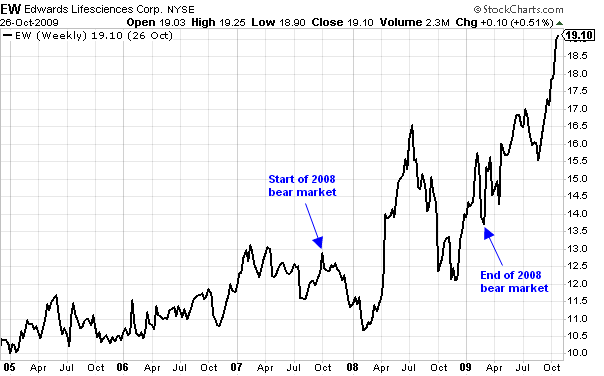

Stock Price RisksThe stock will certainly rally and pullback and continue this pattern as this is what stocks do. But as far as bear markets go, I don't think that Edwards Lifesciences will respond much to a weak economy. To illustrate this, I have shown the stock chart covering the 2008 recession.

Edwards Lifesciences chart by StockCharts.com

As the above chart shows, during the 2008 recession, the stock actually ended the bear market higher than where it started. In fact, the rallies and pullbacks were just part of the general uptrend. Granted, the rallies and pullbacks increased in magnitude, but they were still part of the broader uptrend.

The reason for this trading behavior is linked to the company's products - which are considered to be essential. This means patients will pay for the company's products irrespective of the state of the economy.

ConclusionEdwards Lifesciences has a solid history of growth with more growth expected. The company will release a new medical software product in 2019, which is expected to boost earnings. Management is proactive and capitalizes on opportunities to further boost the company's future growth.

The company is efficiently run and has a history of operating with ample working capital and moderate debt levels, but the stock is expensive with high PEG and PE multiples.

The stock is essentially recession-proof by the nature of its products (which are considered to be essential rather than a luxury). Even though the stock is expensive, I think that Edwards Lifesciences would make a great long-term investment.

Disclosure: I am/we are long EW. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment